Get 50% off on Vault theme. Limited time offer!

Get 50% off on Vault theme. Limited time offer! Types of Company Registration in India 2026: Pvt Ltd, LLP, OPC & More

The idea of opening a new business in India is a delightful expedition, and you can visibly tell from the country’s entrepreneurial ecosystem that the two are in sync. Did you know that by March 2024, the country boasted a total of 2,663,016 registered companies, with 64% of them actively functioning? The new turn to registering more companies than ever before is a clear signal to investors and business owners that there is excellent customer demand and plenty of business opportunities for fresh new entrants!

One of the most ground-breaking decisions a potential entrepreneur has to face is the matter of what legal framework will govern their business. Such a decision decides the entire game from your tax charge and regulatory requirements all the way to your ability to attract investments. On top of that, knowing the different company registration in India not only helps you survive the initial hurdle but also looks after your venture’s ongoing success as well. There are so many different models available, starting from partnership firms to publicly traded companies, that you can pick the perfect one, no matter the size or your dream. Still, sorting through such choices might be quite an ordeal. In this article, we will simplify and explain the seven main types of company registration in India to help you make an informed decision.

What Is Company Registration?

Company registration is the procedure by which any business entity formally joins the ranks of the law under the relevant statutes, mainly the Companies Act, 2013, or the Limited Liability Partnership Act, 2008. By taking this step, a business gains a separate legal entity status from its owners, and therefore, a company can now sign contracts, acquire properties, and even sue or get sued in its own name. It is an official way of filing your business formation with the Registrar of Companies (ROC) or other respective government departments.

Here are some brief points to reflect on:

- Legal Identity: The act assigns the status of a ‘person’ to the business under the law.

- Proof of Existence: The incorporation certificate is the most tangible proof of the business’s legal origin.

- Mandatory Compliance: It subjects the business to a fixed set of statutory rules and reporting obligations.

- Credibility: A registered company is generally more trusted by customers, suppliers, and banks.

Also, it is essential to figure out the right kind of company registration in India from the very beginning, as the structural changes will affect aspects such as liability, capital requirements, and the amount of work involved in administration. Doing it correctly means that your business is not only compliant but also scalable from day one.

Difference between Business Registration and Tax Registration

Both business registration and tax registration are a must if you want to have a clean business operation in India, but they do different things. Understanding this difference is essential for new entrepreneurs.

| Feature | Business Registration (Company/Firm Registration) | Tax Registration (e.g., GST/PAN/TAN) |

| Primary Goal | To establish the legal existence and structure of the entity (e.g., Private Limited Company, LLP). | To obtain unique numbers for tax compliance and reporting purposes (e.g., paying income tax, collecting GST). |

| Administered By | Ministry of Corporate Affairs (MCA) and Registrar of Companies (ROC) or State Registrars. | Income Tax Department (ITD) and Central Board of Indirect Taxes and Customs (CBIC). |

| Legal Status | Grants the business a separate legal identity (for most structures like Pvt Ltd, LLP). | Does not grant a separate legal identity; it’s a number for tracking tax obligations. |

| Key Output | Certificate of Incorporation/Registration. | GSTIN, PAN Card (for the entity), TAN. |

| Applicability | Mandatory for formal structures like OPC, Private Limited, Public Limited, and LLP. Optional for Partnership Firms. | Mandatory based on turnover, nature of business, or income bracket. |

Overview of Business Structures Available in India

The Indian legal framework presents a plethora of business structures to suit the varying needs of a single freelancer to a large-scale enterprise. A decision on which one to use will be influenced by the number of owners, the amount of capital, the owners’ liability preference, and the vision of your future expansion.

These business models can be generally categorised into those with unlimited liability (like Sole Proprietorship) and those with limited liability (like Private Limited Company and LLP). Picking the right one is your very first and most important step out of all the types of company registration in India that you come across. Every choice has its accompanying set of compliance tasks and legal perks.

Why Is Company Registration Essential in India

Registration of a company is not merely a regulatory barrier; it is a tactical step that offers your business operations a robust, legally acknowledged base. It is what actually changes your business from just an idea to a legal entity. The pros of doing company registration in India are:

- Limited Liability Protection: This could be the most significant benefit, whereby the owners’ personal belongings are legally different from the debts of the company, thus protecting them from financial risks.

- More Credibility and Trust: A registered business, especially a Private Limited Company or LLP, shows a professional image, which makes it easier to get customers, suppliers, and potential partners.

- Getting Funding More Easily: Creditors, venture capitalists, and angel investors are willing to provide money to companies that are legally registered, as they have a clear legal position and a good history of compliance.

- Perpetual Succession: Unlike a proprietorship, formal entities such as companies do not cease to exist even if a director or the owner leaves or dies, thus guaranteeing the survival of the business.

- Talent Attraction: Workers usually prefer to be employed by registered and compliant companies, as this indicates that the company is stable and respects labor and other professional laws.

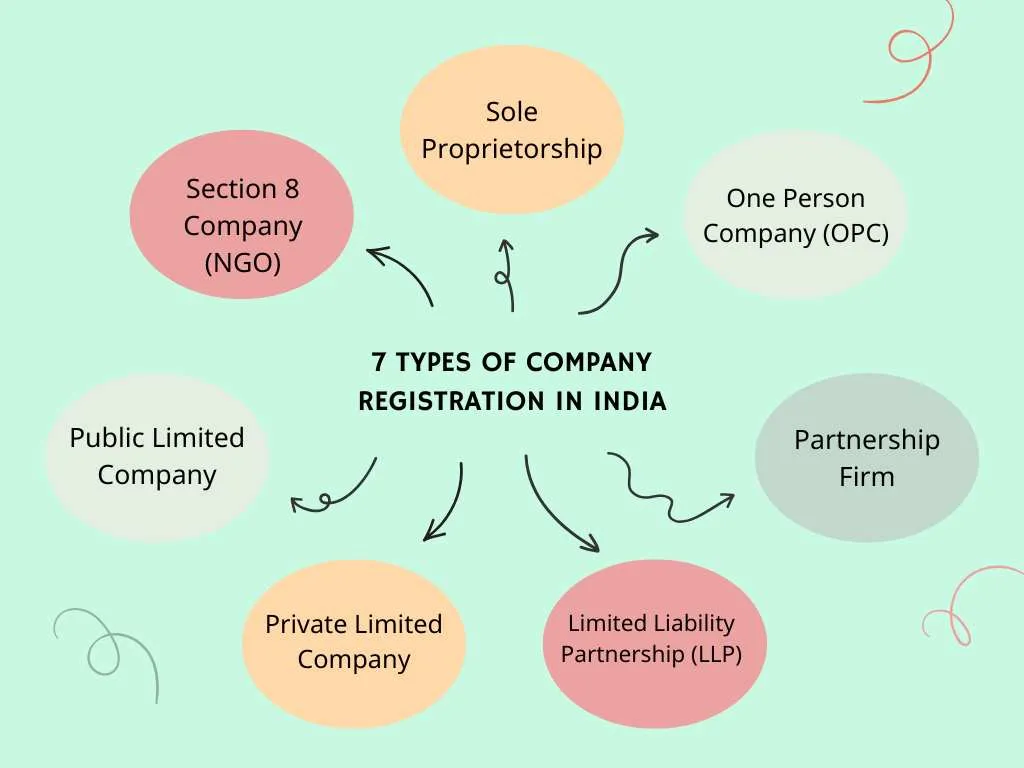

What Are the 7 Types of Company Registration in India?

1. Sole Proprietorship

A Sole Proprietorship is the simplest business form, where the business and its owner are one and the same legally. This kind of business is the simplest to establish and requires very few legal formalities. The owner takes the whole responsibility for the profits, debts, and running of the company. It is usually the first choice of very small-scale businesses, freelancers, and home-based ventures. Besides, the industry is run under the owner’s Permanent Account Number (PAN), which makes the tax system very simple. Moreover, there is no separate Act that governs its creation, as it is not a ‘company’ in the strict legal context.

- Key Benefits: Simple and cheap to establish, low compliance burden.

- Eligibility: Any person, that is, Non-Resident Indians (NRIs) inclusive.

- Advantages & disadvantages: Absolute control, minimal compliance, unlimited liability, raising institutional funding is hard.

- Who should choose it: Single individuals, small traders, freelancers, and independent professionals.

2. One Person Company (OPC)

A One Person Company, introduced as a part of the Companies Act, 2013, is a distinctive concept that permits a single person to operate a formal limited liability business. The person is the owner as well as the director. Alongside the owner, a nominee should be appointed who will take over the owner’s place in case of death or incapacitation. This incorporation offers the benefit of limited liability, just like that of a Private Limited Company, but keeps the sole control intact. Also, the compliance requirement is less compared to that of a Private Limited Company, which makes it a desirable option for a solo entrepreneur.

- Key Benefits: Limited liability for a single owner, single-person control.

- Eligibility: A natural person who is an Indian citizen and a resident in India (stayed in India for at least 120 days in the immediately preceding financial year).

- Advantages & disadvantages: Limited liability, single control, must appoint a nominee, restrictions on converting to other forms.

- Who should choose it: A solo entrepreneur who wants a legal identity and liability protection.

3. Private Limited Company

The Private Limited Company (Pvt Ltd) is one of the most widely utilized types of company registration in India, especially among startups and businesses in the growth phase. Its setup requires at least two directors and two shareholders, and the members’ liability is limited to their shareholding. Besides, its shares are not offered to the public, and there are some limitations on the share transfer. Furthermore, this structure is governed by the Companies Act, 2013, and, therefore, it has the highest scalability potential, which makes it perfect for institutional investments. However, it has a higher compliance burden than an LLP or OPC.

- Key Benefits: Separate legal entity, limited liability, easy to raise equity funding, improved credibility.

- Eligibility: At least 2 Directors, At least 2 Shareholders (can be the same person), One director must be an Indian Resident.

- Advantages & disadvantages: High credibility, easy funding, limited liability, high compliance cost, and requirements.

- Who should choose it: Startups, technology ventures, and businesses seeking investment (Venture Capital/Angel Investors).

4. Public Limited Company

A Public Limited Company is almost the same as a Private Limited Company, but its features aim at large-scale operations. The minimum number of directors should be three, and the members should be at least seven. Also, the company does not have any share transfer restrictions so that it can make an offer to the public, and the shares can be traded on a stock exchange. Furthermore, the degree of compliance and transparency that a Public Limited Company in India requires is at a very high level because it manages public money. However, this type of corporate organization makes it possible to raise a significant amount of capital through public offerings.

- Key Benefits: Public offer of shares (IPO) to raise capital, free transfer of shares, and massive potential for growth.

- Eligibility: Minimum 3 Directors, Minimum 7 Shareholders, no limit on the maximum number of shareholders.

- Advantages & disadvantages: Access to public funds, high liquidity of shares, and a very high compliance and regulatory burden.

- Who should choose it: Large enterprises and companies planning to list on a stock exchange.

5. Limited Liability Partnership (LLP)

Through the LLP Act, 2008, the LLP is a hybrid model combining the best features of a traditional partnership with the limited liability aspect of a company. It has at least two partners, and the liability of a partner is limited to the amount of the contribution specified in the agreement. One partner, however, is generally not held liable if another partner misleads or is negligent. In addition, the LLP compliance requirement is significantly lower than that of a Private Limited Company, which is why the LLP structure is widely accepted among professional firms, consultants, and small and medium-sized enterprises.

- Key Benefits: Limited liability, lower compliance than Pvt Ltd, simple management, and no requirement for compulsory audit if turnover is low.

- Eligibility: Minimum two partners (individuals or bodies corporate), at least one designated partner must be a resident of India.

- Advantages & disadvantages: Limited liability, flexibility, no equity funding, less credibility than a Pvt Ltd Company.

- Who should choose it: Professionals (CA, CS, Lawyers), small partnerships, and service businesses.

6. Partnership Firm

Partnership Firm is a conventional business model involving two or more persons (partners) who execute an agreement to share the profits of a business, which may be carried on by all or any of the partners acting for all. It is regulated by the Indian Partnership Act, 1932. The registration of a partnership firm is voluntary; however, more rights in law accrue to a registered firm. The biggest drawback, though, is the unlimited liability, i.e., the partners’ personal assets may be utilized to satisfy the debts of the firm. Besides that, it is set up through a Partnership Deed that specifies the parts, the duties, and the profit-sharing ratio.

- Key Benefits: Simple and cheap to set up, decision-making by mutual agreement, and minimum regulatory formalities.

- Eligibility: Minimum 2 Partners, maximum 50 partners.

- Advantages & disadvantages: Shared responsibility, easy to set up, unlimited liability, trust-based partnership.

- Who should choose it: Small-scale joint ventures, family businesses, and firms that have no plans for significant external fundraising.

7. Section 8 Company (NGO)

Section 8 Company is a type of non-profit organization registered under the Companies Act, 2013, and established for purposes such as the promotion of trade, industry, art, science, sports, education, research, social welfare, religion, charity, or the protection of the environment. Any profits made go only toward the fulfillment of these objectives and are not distributed as dividends to members. In addition, this organization bears a close resemblance to a Private or Public Limited Company structurally, but with a non-profit motive.

- Key Benefits: Non-profit motive, special legal status, tax benefits for both the donors and the entity.

- Eligibility: Minimum 2 Directors and Shareholders, with the object of promoting art, science, charity, etc.

- Advantages & disadvantages: Tax benefits, high social credibility, restriction on profit distribution, and stringent regulatory oversight of funds.

- Who should choose it: NGOs, Charitable Trusts, Social Enterprises, Trade Associations.

Comparison Table: Types of Company Registration in India

| Feature | Sole Proprietorship | One Person Company (OPC) | Private Limited Company | LLP |

| Ownership | Single individual. | Single owner/shareholder. | Minimum 2 Shareholders. | Minimum 2 Partners. |

| Liability | Unlimited (Owner’s personal assets are at risk). | Limited (Owner’s assets are protected). | Limited (Shareholder liability is limited). | Limited (Partner liability is limited). |

| Compliance | Very Low (Mainly Tax Filings). | Moderate. | High (Annual Filings, Audit, etc.). | Low to Moderate (Audit only if turnover exceeds limit). |

| Best Use Case | Freelancers, very small traders, home-based businesses. | Solo entrepreneurs desiring limited liability. | Startups, high-growth businesses seeking equity funding. | Professional firms, partnerships desiring limited liability and flexibility. |

Which of These Company Registration in India Is the Best? – Based on Business Type

The answer to the question of which type of Indian company registration is the best is different for each person and depends solely on the nature of your business goals, scale, and capital requirements.

- For Solo Businesses with Limited Risk: In case you are the only one in your business but want to protect your liability, a One Person Company (OPC) will work great for you. If you happen to be a tiny business or freelancer, then going for a Sole Proprietorship would be the easiest.

- For Startups Seeking Investment: Nothing comes close to a Private Limited Company. It is the most liked structure amongst the venture capitalists and angel investors mainly because of its well-defined ownership, governance structure, and ease in share issuance.

- For Professional Firms (CA, Legal, Tech Consulting): Limited Liability Partnership (LLP) should be the choice of the majority. GmbH allows the limited liability advantage while keeping the openness and fewer compliance requirements of a partnership structure.

- For Non-Profit/Charitable Activities: A Section 8 Company is the only proper way to get formal registration and, at the same time, enjoy the NPO tax benefits.

Types of Registration Under GST

Goods and Services Tax (GST) registration is a tax requirement that is different from company registration, and it is compulsory based on turnover or the nature of supply. Various registrations available include:

- Regular GST registration: This is for typical businesses whose turnover goes beyond the set limit, and thus they can collect GST and, at the same time claim Input Tax Credit (ITC).

- Composition scheme: A less complicated tax scheme intended for small taxpayers who are required to pay the tax at a fixed percentage of their turnover; however, they are not allowed to claim ITC.

- Casual taxable person: A person who is holding a business in a particular area that doesn’t have a fixed place of business and, in that area, intends to make an occasional transaction, then this person needs a casual taxable person registration.

- Non-resident taxable person: If a non-resident is providing a product or service in India, they should be registered as a non-resident taxable person.

- ISD registration: If a head office receives tax invoices for services and wants to distribute the credit to manufacturing units or service centers, it should have an Input Service Distributor registration.

Pvt Ltd vs LLP vs Sole Proprietorship – Comparison

The comparative analysis of these three popular types of company registration in India exposes the compromises made between liability, compliance, and fundraising potential.

| Feature | Private Limited Company (Pvt Ltd) | Limited Liability Partnership (LLP) | Sole Proprietorship |

| Governing Act | Companies Act, 2013 | LLP Act, 2008 | No specific Act (Operates under other laws). |

| Transferability | Easy (Transfer of Shares). | Difficult (Requires Partner Admission/Cessation). | Not possible (Tied to the owner). |

| Fundraising | Best for Equity Funding (VC/Angel). | Debt-based funding is common (Loans). | Loans in the owner’s personal name. |

| Foreign Investment | Easiest to accept Foreign Direct Investment (FDI). | FDI is permitted, but complex for equity-like contributions. | Difficult/Not possible for FDI. |

| Credibility | Highest. | Moderate to High. | Low. |

| Audit Requirement | Mandatory, regardless of turnover. | Mandatory only if turnover exceeds ₹40 Lakh or contribution exceeds ₹25 Lakh. | Not mandatory (Only as per Income Tax limits). |

Conclusion

Knowing the structure that best fits your needs from the varied kinds of company registration in India is the way to go for a successful and ethically compliant business. If you are one person with a small idea and want to start a Sole Proprietorship or you are a dynamic team with global ambitions and want to set up a Private Limited Company, it is indispensable to have a clear notion of the differences in liability, compliance, and funding capacity. Informed decision-making is a way of ensuring that your venture has the right legal platform for flourishing and expansion.

FAQs

1. What is the minimum number of shareholders required for a Private Limited Company?

The number of shareholders in a Private Limited Company should be at least two and 200 at most.

2. Is it mandatory for a Partnership Firm to be registered in India?

Under the Indian Partnership Act, 1932, registration of a Partnership Firm is optional, but it must be noted that an unregistered firm is not entitled to sue third parties.

3. What is the key advantage of registering as a One Person Company (OPC)?

The main point of OPC registration is that a single individual can enjoy the benefit of limited liability, thereby their personal assets will be safe from business debts.

4. What is the difference in liability between a Sole Proprietorship and an LLP?

A Sole Proprietorship has unlimited liability as opposed to a Limited Liability Partnership (LLP) whose partners have limited liability.

5. Can a Private Limited Company accept foreign investment easily?

Yes, a Private Limited Company is the most suitable vehicle for FDI (Foreign Direct Investment) in India due to its clearly defined set-up.

6. What is the primary purpose of a Section 8 Company?

The main goal of a Section 8 Company is to facilitate the promotion of non-profit activities, for example, art, science, and social welfare, etc., and to use all profits for the said purposes.