The financial environment in India is changing rapidly, and emergency cash has never been easier to come by. Be it a medical bill that came out of the blue, a sudden need to fix your house, or even a paycheck that won’t meet your needs at the end of the month, 7-day loan applications provide immediate solutions to your problems right at your fingertips. These platforms use AI-based credit scoring, low KYC requirements, and bank-integrated disbursements to issue loans in minutes, not days.

Unlike traditional banks, which require extensive paperwork and long queues, modern lending applications have democratised short-term lending for salaried professionals, students, and the self-employed alike. As there are more than 500 million users of smartphones in India and fintech usage is higher than ever, this guide includes the best 7 day loan app list, their state of registration by RBI, interest rates, eligibility, red flags to avoid, and safety tips, everything you need to borrow smartly and safely in 2026.

What is a 7-Day Loan?

A 7-day loan is a very short-term financial product designed to provide direct financial relief in the form of quick cash to cover urgent needs. These loans are small-value credits of between 500 and 50,000 rupees, designed to be repaid within 7 days of issuance. Unlike traditional bank loans, which can take weeks or months to be approved, 7-day loans are approved and disbursed in hours and are therefore suitable when one is in dire need.

If you’re looking for quick options, exploring a 7 Days Loan App List can help you identify trusted platforms that provide these short-term loans with minimal hassle.

The rationale of a 7-day loan is based on the increasing demand of micro-financing services that address the mismatch between the emergency financial needs and the fixed finance cycles. Such loans can be especially helpful to people who get a salary and can experience short-term financial problems before the next pay. The small repayment period makes sure that the borrowers are not caught in long cycles of debt as well as immediate financial assistance. These loans can also serve as a loan app for students who need quick cash for emergencies without complex approval processes.

Majority of 7-day loans are based on a simple-interest model with fixed fees so that the borrowers are able to know in advance how much they will pay. These loans are appealing to traditional banking products for their fast processing times, low documentation requirements, and immediate disbursement when quick funds are required.

What are “7 Days Loan Apps”?

7-day loan apps are mobile applications designed to offer short-term lending services on smartphones. Such online platforms have transformed the lending industry by making the lending process more convenient: physical documents are no longer required, processing times are shorter, and credit is available to a wider range of the population. On the 7 Days Loan App List, there are many fintech companies that have created advanced algorithm-based solutions to evaluate creditworthiness based on alternative data.

Such applications usually do not demand much documentation, sometimes it just needs users to fill in the basic personal information and income details and also access their bank accounts so that it can carry out necessary checks. These apps are easy to use and accessible to people with varying levels of technical skill. The borrowing process has become easy and transparent with features such as instant KYC verification, automated EMI deductions as well as real-time loan tracking. Most of the apps also have other options such as expense tracking, financial planning and credit check to enable proper management of their accounts.

Why Short-Term Loans are Gaining Popularity in India

- Technology Revolution: Smartphones have made it possible for a new generation of consumers to enjoy financial services, unlike the banking system before. With an internet population of 750 million, these digital lending platforms can very well serve customers in far-flung rural areas where branch networks are scarce.

- Instant Gratification Culture: The modern-day consumer expects instant solutions to their problems. 7 day loan apps meet this expectation of theirs and provide instant loan approvals and disbursal whereas traditional banks will take their own sweet time, sometimes weeks.

- Simplified Documentation Process: Bank loans, meanwhile, come with loads of paperwork, income proofs, and guarantors. Short-term loan apps have developed a simple digital solution requiring only basic KYC documents and bank statements to verify identity.

- Flexible Repayment Options: The repayment options on these apps range from auto-debit to manual UPI transfers to selecting from several digital wallets, giving users an easy way to repay loans without attending a physical location.

- Credit Score Improvement: Most apps under 7 days loan app list report repayment history to credit bureaus and credit agencies, thereby building or improving credit score for the users by repaying on time.

Eligibility Criteria for 7-Day Loans

- Age Restrictions: Most lending apps allow users to borrow between the age of 21 to 65, which ensures that they have an actual legal chance of entering into financial contracts and earning in the future.

- Income Verification: Applicants are usually required to present a consistent stream of monthly deposits through their salary slips, bank statements, or other income declaration documents such as tax returns, often with a baseline of ₹15,000-₹25,000.

- Employment Status: Primarily unsalaried individuals constitute freelancers and self-employed people with proof of stable earnings. Hence, these lending applications prioritize those with salaried employment and traditional job stability.

- Credit Score Evaluation: Many lenders do not consider credit scores an absolute requirement for granting loans. However, having good (650+) will favorably impact the chances of getting loans, along with the terms applicable to them.

- Bank Account Requirements: For verification purposes, bank accounts must not only be active but also require bank statements covering >3-6 months for automated loan repayment systems and detailed clearing services.

- Residential Proof: Providing user numbers alongside address proof helps validate borrowers’ claims while helping loan providers serve loans accurately and automating collections.

Top 10 Best 7 Days Loan App List in India (2026)

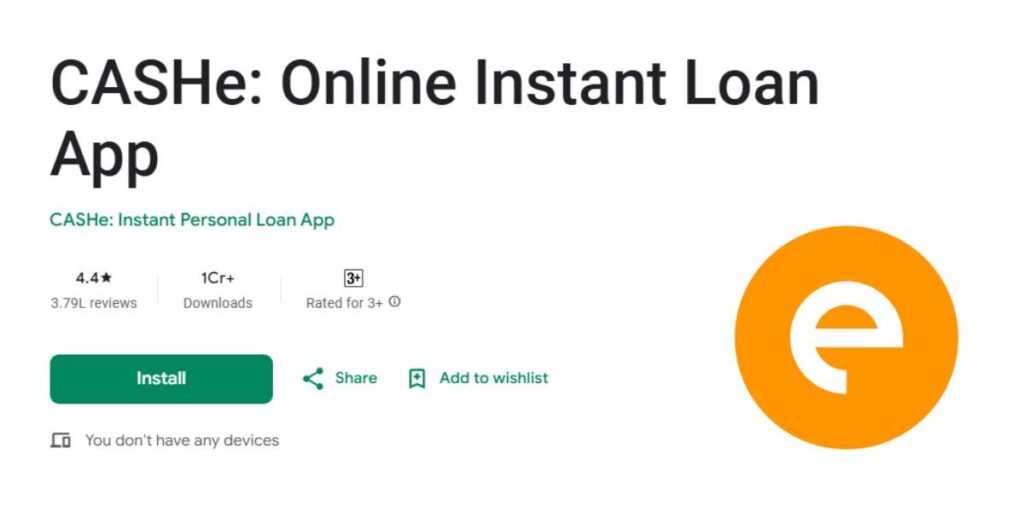

1. CASHe

CASHe is among the most well-known digital lending platforms in India, exclusively focused on young professionals and millennials needing fast financing options. The application leverages new credit evaluation practices, such as social media and spending habits, to assess loan applicants. CASHe is a lending platform that has lent over 1,000 crores to 2 million+ customers across India, with an easy-to-use interface and fast processing. It also features prominently in many 7 Days Loan App List recommendations due to its quick disbursement and minimal documentation.

Loan Amount: ₹10,000 to ₹4,00,000

Interest Rate: 2.25% per month onwards

Eligibility: Salaried professionals aged 23-58 with minimum ₹20,000 monthly income

Pros:

- Instant loan approval within 8 minutes

- Flexible repayment options up to 24 months

- No hidden charges or prepayment penalties

- Credit line increases with good repayment history

Cons:

- Limited to salaried employees only

- Higher interest rates for new customers

- Strict income requirements may exclude many applicants

- Limited customer support during peak hours

Download Link: https://play.google.com/store/apps/details?id=co.tslc.cashe.android&pcampaignid=web_share

2. KreditBee

KreditBee has become a full-fledged financial services provider that provides a wide range of loan products such as short-term individual loans. The app will take advantage of superior artificial intelligence and machine learning to deliver real-time credit decisions. KreditBee has more than 10 million downloads and is well established in India and has competitive interest rates and flexible repayment schemes depending on the needs of the individual customers. It is also frequently mentioned in the 7 Days Loan App List for its quick loan disbursal and user-friendly process tailored to short-term borrowers.

Loan Amount: ₹1,000 to ₹5,00,000

Interest Rate: 1.5% per month onwards

Eligibility: Indian citizens aged 21-55 with verified income source

Pros:

- Wide loan amount range suitable for various needs

- Competitive interest rates compared to other apps

- Multiple repayment tenure options available

- Strong customer support and grievance resolution

Cons:

- Lengthy verification process for first-time users

- Limited availability in certain pin codes

- Higher processing fees for smaller loan amounts

- Strict repayment terms with penalty charges

Download Link: https://play.google.com/store/apps/details?id=com.kreditbee.android&pcampaignid=web_share

3. LazyPay

LazyPay has changed the idea of instant credit by providing a digital credit line that individuals can utilize on various platforms and merchants. LazyPay offers a flexible spending limit in contrast to conventional loan apps where it is possible to use the sum of money on different purchases and repay in installments. The application is connected to the most famous e-commerce websites, food delivery services, and utility payment systems. Due to its quick approval process and convenience, LazyPay is often included in the 7 Days Loan App List as a reliable option for short-term credit needs.

Loan Amount: ₹500 to ₹1,00,000 credit limit

Interest Rate: 1.75% per month for EMI conversions

Eligibility: Working professionals aged 22-45 with stable income

Pros:

- No interest on pay-by-month options

- Wide merchant network acceptance

- Flexible spending across multiple categories

- Easy EMI conversion facility available

Cons:

- Limited to specific merchant partnerships

- Credit limit increases gradually over time

- Late payment penalties can be substantial

- Not suitable for cash requirements

Download Link: https://play.google.com/store/apps/details?id=com.citrus.citruspay&pcampaignid=web_share

4. NIRA

NIRA specialises in offering small-ticket lending to salaried people with high emphasis on digital innovations and customer experience. The app applies its own proprietary algorithms to evaluate creditworthiness and provides customised loan products. The advantage of NIRA is that it has a simple application procedure and pricing, which means that even a first-time borrower can easily access it.

Loan Amount: ₹5,000 to ₹2,00,000

Interest Rate: 2% per month onwards

Eligibility: Salaried employees aged 21-60 with minimum ₹15,000 monthly income

Pros:

- Simple and quick application process

- Transparent fee structure with no hidden charges

- Flexible repayment options available

- Good customer service and support

Cons:

- Limited loan amounts for emergency needs

- Higher interest rates for new customers

- Strict employment verification requirements

- Limited availability in smaller cities

Download Link: https://play.google.com/store/apps/details?id=com.nirafinance.customer&pcampaignid=web_share

5. PaySense

PaySense has positioned itself as a trusted personal lending platform that targets the emerging middle, with a keen interest in serving the emerging middle. The app also provides competitive interest rates and flexible repayment term, which makes it usable in diverse financial requirements. The major strength of PaySense is that it has a holistic credit evaluation procedure and customized loans according to personal profiles. Due to its fast disbursal and ease of access, PaySense is often mentioned in the 7 Days Loan App List for users seeking quick and reliable credit solutions.

Loan Amount: ₹5,000 to ₹5,00,000

Interest Rate: 1.17% per month onwards

Eligibility: Salaried/self-employed individuals aged 25-55

Pros:

- Competitive interest rates in the market

- Flexible repayment tenure up to 60 months

- Both salaried and self-employed individuals eligible

- No collateral or guarantor required

Cons:

- Lengthy documentation process initially

- Credit score requirements may be strict

- Processing time longer than instant loan apps

- Limited customer support availability

Download Link: https://play.google.com/store/apps/details?id=com.gopaysense.android.boost&pcampaignid=web_share

6. Stashfin

Stashfin also has a special credit line facility which allows the user to get immediate access to funds as and when required. The app is concerned with developing long term customer relationships by ensuring responsible lending policies and competitive pricing. The innovative approach implemented by Stashfin offers such features as expense tracking and financial planning tools in addition to lending services.

Loan Amount: ₹1,000 to ₹5,00,000

Interest Rate: 0% interest for first-time users (limited period)

Eligibility: Working professionals aged 18-65 with regular income

Pros:

- Interest-free loans for eligible first-time users

- Instant credit line approval and activation

- No prepayment penalties or hidden charges

- Additional financial management tools included

Cons:

- Limited promotional offers for existing customers

- Credit limit enhancement takes time

- Strict repayment monitoring with penalties

- App interface could be more user-friendly

Download Link: https://play.google.com/store/apps/details?id=com.stashfin.android&pcampaignid=web_share

7. MoneyView

MoneyView has created a niche in the digital lending industry with the help of personalized financial services offering underpinned by sound technological infrastructure. The application offers a full range of loan products on competitive terms and is aimed at financial inclusion of underserved segments. One of the strengths of MoneyView is that it employs a data-driven approach to credit score and customer service. Its quick loan disbursal process and simplified user experience have earned it a place in many 7 Days Loan App List recommendations for fast and reliable short-term credit options.

Loan Amount: ₹5,000 to ₹10,00,000

Interest Rate: 1.33% per month onwards

Eligibility: Salaried/self-employed individuals aged 23-58

Pros:

- High loan amounts available for qualified applicants

- Comprehensive financial services beyond lending

- Strong technology platform with security features

- Dedicated relationship manager for high-value loans

Cons:

- Higher documentation requirements

- Longer processing time for loan approval

- Limited availability in tier-3 cities

- Minimum income requirements may be restrictive

Download Link: https://play.google.com/store/apps/details?id=com.whizdm.moneyview.loans&pcampaignid=web_share

8. mPokket

mPokket focuses on students and younger professionals with low-value loans that are sold to cover immediate consumption. Their niche is the younger population, and the app specializes in providing loans to cover education plans, lifestyle requirements, and emergency needs. The simplified interface of the app allows even users with a poor credit history to use their services.

Loan Amount: ₹500 to ₹30,000

Interest Rate: 1.25% per month onwards

Eligibility: Students and working professionals aged 18-29

Pros:

- Specifically designed for young users

- Lower minimum loan amounts available

- Simple application process for students

- Quick disbursal within few hours

Cons:

- Limited loan amounts for larger needs

- Age restrictions limit customer base

- Higher interest rates compared to traditional loans

- Limited repayment flexibility options

Download Link: https://play.google.com/store/apps/details?id=com.mpokket.app&pcampaignid=web_share

9. Olyv

The brand Olyv specialises in delivering speedy personal loans and prioritises the customer experience as well as open lending policies. The application has competitive tariffs and reasonable conditions along with high adherence to regulatory standards. The strategy involves an integration of technology and human touch and this is what will enable Olyv to provide personalized lending. Due to its fast processing and customer-centric features, Olyv is often mentioned in the 7 Days Loan App List for users seeking instant short-term credit.

Loan Amount: ₹10,000 to ₹2,00,000

Interest Rate: 2.5% per month onwards

Eligibility: Salaried employees aged 25-55 with stable employment

Pros:

- Transparent pricing with clear terms

- Personalized loan offers based on profile

- Strong regulatory compliance and security

- Flexible repayment scheduling options

Cons:

- Limited marketing presence compared to competitors

- Slower loan processing than instant apps

- Higher minimum loan amount requirement

- Strict eligibility criteria may exclude applicants

Download Link: https://play.google.com/store/apps/details?id=in.rebase.app&pcampaignid=web_share

10. EarlySalary (Now Fibe)

EarlySalary was the first to introduce the concept of salary advance loans in India and enables employees to access their earned but unpaid salary. Its app provides a distinctive value offer because it proposes to lend money as an advance in salary, rather than a conventional credit instrument, making it psychologically less difficult to be responsible when borrowing.

Loan Amount: ₹5,000 to ₹5,00,000

Interest Rate: 2.5% per month onwards

Eligibility: Salaried employees aged 23-55 with 6 months job stability

Pros:

- Unique salary advance concept

- Integration with employer payroll systems

- Lower default rates due to salary linkage

- Educational content on financial literacy

Cons:

- Limited to salaried employees only

- Employer partnership required for better terms

- Higher interest rates for non-partnered companies

- Limited loan amounts for new users

Download Link: https://play.google.com/store/apps/details?id=com.earlysalary.android&pcampaignid=web_share

Without CIBIL Score Options

A number of 7-day loan apps provide loans to individuals with a low or no CIBIL score based on other data:

- mPokket: Accepts students and first time borrowers, no CIBIL required.

- KreditBee: is AI-based credit score; CIBIL is not required on small loans.

- CASHe: Evaluates social behaviour and income patterns instead of CIBIL

- Stashfin: Provides credit lines to thin credit files users.

- Nira Finance: Takes into consideration salary credits and bank statements in preference to CIBIL.

- PaySene: Allows low-CIBIL borrowers on the basis of employment and income security

- EarlySalary (Fibe): Salary-based advances; CIBIL score is not a key factor.

- LazyPay: Credit evaluation based on the spending patterns and online footprint.

Comparison Table

| App Name | Loan Amount | Interest Rate | Processing Time | Ratings |

| CASHe | ₹10,000 – ₹4,00,000 | 2.25% per month | 8 minutes | 4.2/5 |

| KreditBee | ₹1,000 – ₹5,00,000 | 1.5% per month | 15 minutes | 4.3/5 |

| LazyPay | ₹500 – ₹1,00,000 | 1.75% per month | Instant | 4.1/5 |

| NIRA | ₹5,000 – ₹2,00,000 | 2% per month | 10 minutes | 4.0/5 |

| PaySense | ₹5,000 – ₹5,00,000 | 1.17% per month | 30 minutes | 4.4/5 |

| Stashfin | ₹1,000 – ₹5,00,000 | 0% (promotional) | 5 minutes | 4.2/5 |

| MoneyView | ₹5,000 – ₹10,00,000 | 1.33% per month | 24 hours | 4.3/5 |

| mPokket | ₹500 – ₹30,000 | 1.25% per month | 2 hours | 4.0/5 |

| Olyv | ₹10,000 – ₹2,00,000 | 2.5% per month | 45 minutes | 3.9/5 |

| EarlySalary | ₹5,000 – ₹5,00,000 | 2.5% per month | 20 minutes | 4.1/5 |

How to Apply for a 7-Day Loan Online

The procedure of signing up for a 7-day loan using mobile apps has been simplified to the maximum to guarantee the highest degree of convenience and rapidity. Start by installing your preferred app in the 7 days loan app list found in Google Play Store or Apple App Store. Register with your mobile number and fill in the simple registration form such as email verification.

Fill in your profile and include the necessary personal data like full name, date of birth, permanent address, and the address of the current residence. Upload the necessary documents, such as an Aadhaar card, a PAN card, and a recent passport-size photograph. OCR technology is applied in most apps to automatically extract information contained in documents and minimizes the use of manual data entry.

Connect your bank account by entering account details or net banking credentials to get verified immediately. The application will evaluate your purchase records to determine your income trends and expenditure pattern. Ensure you grant the app adequate permissions to secure and prevent fraud using the data on your device.

Choose the loan amount and repayment period of your choice according to your needs. Check the interest rate, processing fees and the amount you will have to pay back, prior to making your application. The majority of applications provide a quick approval verdict, and the funds are usually released to your connected bank account within 15-30 minutes of approval.

Other Cost to Watch Out For

- Processing Charges: Most apps charge a processing fee of 1-5% of the loan amount, usually deducted from the disbursed amount. Do check whether this is refundable in case of early repayment.

- Late Payment Penalties: Late or delayed repayments attract stiff penalties that can go up to ₹500-₹1,000 per day plus interest on the outstanding amount. Such penalties aggravate the total debt load.

- Bounce Charges: Bounce charges may be levied for EMI payments that could not be processed due to insufficient funds, generally between ₹300-₹750 for each failed transaction. Multiple bounces may also negatively affect your credit score.

- Conversion Fees: Some apps may charge a fee to convert lump-sum repayments into EMIs or to extend the repayment period. These charges further increase the overall cost of borrowing.

- Prepayment Charges: This varies. While most apps do not charge for prepayments, some may levy foreclosure charges for early repayment in case of mid or long-term tenure based loans. Do check the terms and conditions for this before you borrow.

- Hidden Service Charges: Also beware of additional charges such as SMS fees, statement generation charges, or account maintenance fees that may be prominently displayed during the application process.

Pros & Cons of 7-Day Loan Apps

Pros:

- Instant Loan Processing and Approval: Most apps offer lending approval within a few minutes, which suits an emergency when need for money comes in need of immediate relief.

- Few Paperwork Requirements: In contrast to traditional banks, different applications ask for just a handful of documents; with such, the process of applying has become very straightforward and accessible to a larger population.

- Availability: These digital platforms work 24/7, thus providing lending services at all hours including weekends and holidays when banks let loose.

- Physical Appearance Not Required: No more physical visits for application or for disbursal either; everything takes place on the Internet.

- Transparent Pricing Structure: Most apps display interest rates, processing fees, and repayment amount upfront to ensure borrowers know what they are committing to.

- Improves Customer Credit Standing: Timely repayment helps develop positive credit history for customers with the potential of affecting the ability of customers to borrow in better amounts and terms.

Cons:

- Higher Interest Rates: Short-term loans usually have higher interest rates compared to traditional bank loans, and so the cost of borrowing increases tremendously.

- Risk of Debt Trap: Easy accessibility to credit may encourage impulsive borrowing, potentially entrapping users in debt cycles if not correctly managed.

- Limited Loan Amounts: Most apps offer small loan amounts that may not be suitable for major financial emergencies or big expenses.

- Harsh Repayment Terms: A short repayment period leaves little wiggle room for varying financial difficulties and income delays on the part of the borrower.

- Data Privacy Concerns: These apps require accessing a lot of personal and financial data, leading to possible privacy and security concerns regarding the highly sensitive information.

- Hidden Charges Risk: Some apps may include additional fees or charges that aren’t disclosed beforehand, possibly increasing the apparent cost of the loan.

How to Verify a Loan App

To avoid downloading any loan app, follow the steps to ensure it is legit:

- Check RBI Registration: Go to the website rbi.org.in and navigate to the NBFC/NBNFC registry to ensure that the lender is registered.

- Google Play Store search: Find the name of the developer, verified badge, downloads (more than 1 million = more reliable), and reviews (read them).

- Check NBFC Partner: Authorized apps will list their lending NBFC partner on their site or in the app’s About section.

- Check Grievance Redressal: A valid loan application should display the name of a nodal officer, an email address, and a physical address, as per RBI requirements.

- App Permissions: Deny any application that wants to access contacts, camera or SMS beyond what is required in KYC verification.

- Check the presence of SSL and a Privacy Policy: The app’s site must use HTTPS and include a clear Privacy Policy and Terms and Conditions page.

- Search the RBI caution List: RBI regularly publishes lists of unregistered online lenders; verify before using.

- Check Loan Agreement: A valid lender would always provide a signed electronic loan agreement before disbursing funds.

Risks of 7-Day Loan Apps

- Extremely High Interest Rates: APRs on 7-day loans can exceed 300–500%, making them far costlier than traditional loans if not repaid promptly.

- Debt Trap Risk: The ease of rollovers or reborrowing can quickly turn small loans into unsustainable debt cycles.

- Privacy Invasion: Privacy: A lot of unverified apps require access to contacts, photos, and SMS information, which can be abused to harass in the recovery process.

- Hidden Fees: Bouncing and processing fees, as well as interest as a penalty, are usually covered in the fine print, making the overall repayment amount large.

- Predatory Recovery Tactics: Unlicensed apps often employ forceful, abusive, and unlawful recovery approaches such as calling family members or employers.

- Risk of Data Theft: Aadhaar, PAN, and banking details are stolen through fraudulent apps that replicate legitimate platforms and use them to commit identity theft and financial fraud.

Safe Alternatives to 7-Day Loan Apps

- Credit Card Cash Advance: Instant cash at reduced effective rates; best when you have a credit card with an available limit.

- Employer Salary Advance: Ask your HR department to advance your salary; no interest and no paperwork.

- Family or Friend Loan: The family or friend loan is interest-free, short-term, requires no credit check, no application, and poses no risk of misuse of data.

- Bank Overdraft Facility: Customers with existing accounts can get pre-approved interest-charged overdrafts at the bank.

- Government PM SVANidhi Scheme: A micro-loan scheme supported by the RBI that offers low-income earners and street vendors collateral-free micro-loans.

- NBFC Personal Loan: NBFCs such as Bajaj Finance are licensed and provide personal loans in a regulated manner, with the appropriate documentation.

- Gold Loan: Collateralize gold jewels to get instant cash at low-interest rates provided by banks or Muthoot/Manappuram Finance.

- P2P Lending Platforms: Faircent, which is regulated by the RBI, is a short-term credit service offering competitive peer-to-peer rates.

Final Thoughts – Should You Use a 7-Day Loan App?

A 7-day loan application can be a helpful financial tool in case one knows how to use it and apply it to a real emergency. The 7 days loan app list are competitive since they are convenient, fast and reachable in urgent financial situations as compared to traditional banking products. The high interest rates and short repayment periods, however, need to be carefully considered and managed from a financial perspective.

This type of app is most appropriate for people with regular sources of income who need temporary funding in case of cash flow gaps. The secret to effective use is to borrow only what you can repay over the given period, and not to be tempted to borrow for what you do not need to spend money on.

Conduct thorough research, compare offers, and select the 7-day loan app with clear pricing, positive customer feedback, and sound regulatory practices. It is important to remember that these loans are not meant to replace adequate financial planning and the accumulation of emergency funds, which are the hallmarks of long-term financial stability.

Common FAQs

What loan application offers money within 7 days?

Loans Apps such as KreditBee, CASHe, Stashfin, LazyPay and mPokket are disbursed within minutes of approval – most within 15-30 minutes. The funds are deposited in your bank account immediately after application, so they are perfect when you need them within 7 days to make a repayment.

Are the 7-day loan apps approved by the RBI?

Not all of them. KreditBee, PaySense, MoneyView, and EarlySalary are legitimate platforms that work with NBFCs registered by the RBI. Nevertheless, there are numerous unregistered illegal apps. Always check on rbi.org.in prior to applying.

What is the interest rate of the 7-day loans?

Verified apps are usually charged between 1.17% and 2.5% per month (around 14% and 30% per annum). But the effective cost per day on a 7-day loan is high, and should always be calculated before borrowing.

What are the ways to prevent loan application scams?

Check RBI/NBFC registration, do not install apps that require complete contact information, do not pay an initial fee, check Google Play reviews, have a physical address and a grievance officer, and report suspicious apps to cybercrime.gov.in or the RBI Sachet portal.

What is the lowest credit score on 7-day loans?

The majority of apps are not as picky about credit scores, though a score of 650 or higher will improve the odds of approval and may lead to a lower interest rate.

How quickly do I need to receive the loan amount in my bank account?

Most often, when a loan is approved, it is disbursed within 15-30 minutes, but some applications can take up to 24 hours due to banking partnerships.